Let’s say that cashlessness is coming–that physical money goes the way of all flesh and electronic money takes over.

OK. So, that’s that. Now, who will issue our money? Someone? Anyone? No one? The structure we have now, in which commercial banks create credit money under the jurisdiction of central banks, is not a law of nature like gravitational waves or the phases of the moon. It’s just the way we organized monetary affairs at a particular moment in time. That moment in time may be coming to an end.

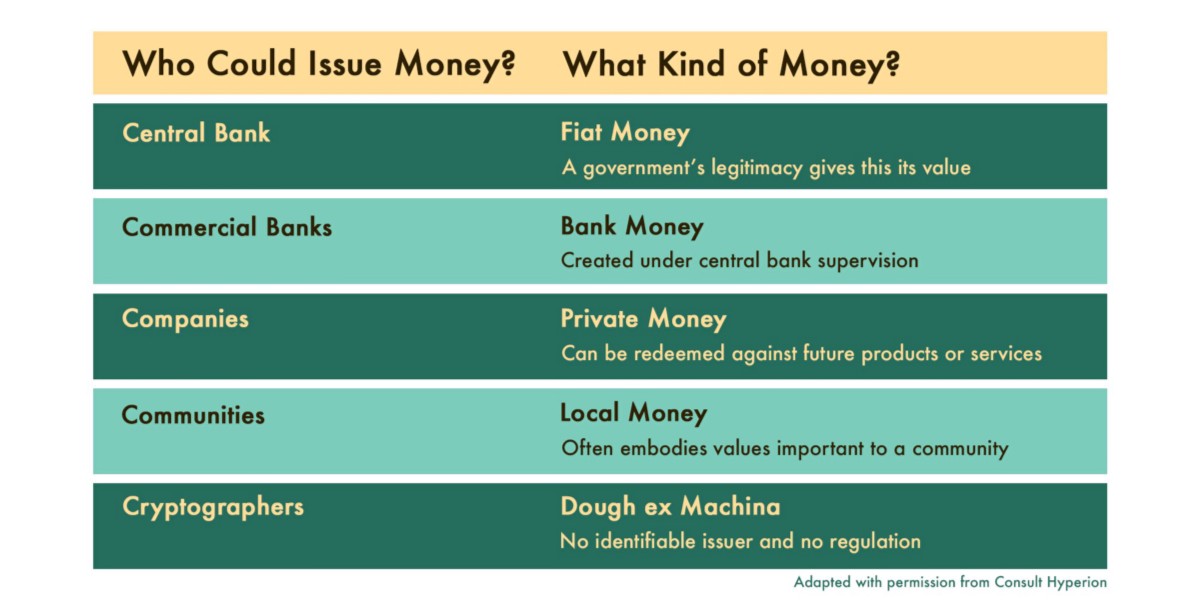

For the purposes of discussion, let’s say there are five broad categories of potential money-issuers, and therefore five broad categories to explore. Take a look.

Fiat Money

Are central banks artifacts of the Industrial Revolution, like canal networks or newspapers, or are they indispensable? I tend to think sophisticated societies didn’t used to have them and we won’t have them in the future. One thing’s for certain, though: If central banks don’t replace physical cash with their own electronic equivalent, they’ll essentially do little more than supervise the privatization of currency.

This recent Positive Money report on “digital cash” provides an excellent review of the issues associated with a central-bank alternative to physical currency. Ultimately, it recommends that central banks issue digital money for six main reasons:

- to widen the range of options for monetary policy (including removing the zero lower bound on interest rates),

- make the financial system safer,

- encourage innovation in the payment system,

- recapture a portion of seigniorage,

- develop alternative finance businesses,

- and improve financial inclusion.

To see a practical example of a central bank already thinking along these lines, look to China. The governor of the People’s Bank of China, Zhou Xiaochuan, explained the bank’s current thinking around adopting a digital currency in an extensive interview at the beginning of 2016. Noting an “irresistible trend” that will see paper money “replaced by new products and new technologies,” the governor set some broad parameters for how a digital currency might operate in China: “A digital currency should be designed in a way that can best protect people’s privacy, but we also need to pay attention to social security and social order.”

Xiaochuan estimated it will take about 10 years for a digital currency to fully replace cash in China, anticipating a period of transition where digital and physical currency will coexist. For now, he has plans to gradually phase out paper money–to start, the costs for cash transactions will increase as banks begin charging fees for any accounting related to physical cash.

Bank Money

Commercial banks could issue their own money, of course, just as they once did. At the time of the American Civil War, there were 1,600 state banks issuing some 30,000 different banknotes. The argument for this kind of private money owes its recent development to economists belonging to what is known as the “Austrian School” of economic thought. Back in the 1970s, Nobel Prize-winning economist Friedrich Hayek presented the case for a diverse monetary base in which private banks would continue to create money through credit but apart from a national currency; as in, each would issue their own money.

Hayek proposed that private currency would be more likely than nation state currency to produce sound money–not liable to sudden appreciation or depreciation in value–because issuers of private currency would have to compete to keep the value of their currency up. It was an interesting thought experiment at the time, but it was difficult to see it as anything more. Hayek himself discussed the practical barriers, noting the problem of how cash registers or vending machines would handle notes and coins of differing denominations, size, or weight, whose relative values would fluctuate. He did, however, foresee this:

Another possible development would be the replacement of the present coins by plastic or similar tokens with electronic markings which every cash register and slot machine would be able to sort out, and the “signature” of which would be legally protected against forgery as any other document of value.

Those “tokens with electronic markings” Hayek predicted? I’m quite certain they’re the mobile phones we have now.

Private Money

Assuming we don’t see central banks switch to digital currencies or commercial banks issue their own money, could the invention of digital monies shift elsewhere? I think so.

The link between banking and payments is weakening. In fact, there has never been any sound reason why a single institution should perform both the functions of lending and payments. Organizations other than banks are perfectly capable of handling the latter, and there is every reason to encourage a richer ecology in the payments world.

The lateral thinker Edward de Bono explored the issue of private company money as far back as the 1990s in a fascinating pamphlet for the Centre for the Study of Financial Innovation (CSFI), a London-based financial services think tank. (He also discusses it in David Boyle’s excellent book The Money Changers.) His central point was that if the cost of issuing currency fell, it would make economic sense for companies to issue their own money, rather than use equities. He wrote that he looked forward to a time when “the successors to Bill Gates will have put the successors to Alan Greenspan out of business.”

In effect, de Bono argued that companies could raise money just as governments do now–by printing it. He pitched the idea of private currency as a claim on the future products or services produced by the currency-issuer. So, IBM might issue “IBM dollars,” a currency redeemable for IBM products and services but also practically tradable for other companies’ monies or assets. To make a scheme like this work, IBM would need to manage the supply of its money to ensure that inflation did not destroy the value of its future products and services–as with, for example, too many vouchers chasing too few goods. But companies should be able to manage that trick at least as easily as governments do, particularly as they don’t have to cope with the input of a nation of voters.

With millions or even tens of millions of these company currencies in circulation, constantly being traded on foreign exchange markets, this all might sound like it would be too unbearably complex for anyone actually trying to pay anyone else. But remember, this would not be analogous to me taking banknotes out of my wallet and handing them to you. This would be my computer (or more likely my mobile phone), talking to your computer (or more likely your mobile phone). Our mobile phones are entirely capable of negotiating between themselves to work out a deal. In his original work, de Bono wrote:

Pre-agreed algorithms would determine which financial assets were sold by the purchaser of the good or service according to the value of the transaction. And the supplier of that good or service would know that the incoming funds would be allocated to the appropriate combination of assets as prescribed by another pre-agreed algorithm. Eligible assets will be any financial assets for which there were market clearing prices in real time. The same system could match demands and supplies of financial assets, determine prices and make settlements.

I also wrote about this in more detail for the Financial Times back in 2014, pointing out de Bono’s emphasis on “the ability of computers to communicate in real time to permit instantaneous verification of the creditworthiness of counterparties” as key to this kind of system. It was an early vision of the reputation economy I investigated further in my book Identity Is the New Money.

Local Money

While there is a tradition of looking at social, alternative, and complementary monies as a means to achieve social good, it has been at the margins of economic thinking. However, the idea of using community-based money to create economic activity where there is none–set out in, for example, Bernard Lietaer’s 2001 book The Future of Money–is very attractive, and we’ve seen a great many related experiments around the world.

The global financial crisis has given the issue of community money ever more renewed thrust. The absence of conventional money in countries such as Italy and Greece has pushed communities into thinking more radically. It may be tempting to belittle alternative currencies as limited, unrealistic, or even a little kooky, but they do work–so long as they don’t run into counterfeiting problems and supply is intelligently controlled to avoid inflation.

I can even see promise for multiple community currencies. While a global currency across all towns or cities is more efficient for transactions, it stops economic managers from tailoring the institutions of money to local circumstances–hence the attractive notion of smaller subset communities tied to specific currencies, minimizing transaction costs between members. Dividing alternative currencies into local and global tends to privilege the local, and there is evidence to support the idea that local currencies are better suited to support growth within communities, largely because they mitigate against hoarding (which plagues the nascent Bitcoin economy).

Douglas Rushkoff, writing in The Atlantic this month, said that the “simplest approach to limiting the delocalizing, extractive power of central currency is for communities to adopt their own local currencies.” But more than economic efficiencies, community currencies may embody values (e.g., environmental policies) that are important to a specific population and therefore drive usage. For example, one might imagine a gold-backed currency for the Islamic diaspora (a non-interest bearing Sharia-compliant option for a billion people) or a renewable energy currency for the green movement (based on future kilowatt hours).

Dough ex Machina

The final category of plausible future money-issuer is, essentially, nobody. The advent of Bitcoin and other cryptocurrencies has opened up the possibility that tomorrow’s currency may be intrinsic to its technology–and beyond human control, insofar as it extends to issuing.

It is always interesting to speculate about what this might mean for the political economy in coming generations. First, if money is placed beyond political control, we’ll see a return to a sort of “electronic gold standard” where communities have very limited options for responding to changing economic circumstances. Second, if new cryptocurrencies exploit the technological potential to deliver the anonymity of cash on a global scale, one might imagine that the rich and powerful will adopt them enthusiastically in an effort to remain beyond any reach of democratic accountability.

Neither of these visions seem particularly appealing to me. On the other hand, the interaction of multiple, overlapping currencies beyond political control that create an environment much more resistant to shocks and chaos may have something to it. The idea of a richer money ecology has its benefits.

Given our experiences to date, it seems to me that the technology of cryptocurrencies–for one, the smart contracts of the blockchain–will have widespread application. The new technology finally provides a way to implement smart contracts–computer protocols that facilitate and enforce fulfillment of contracts developed back in 1997 by Nick Szabo–on a large scale. Whether it will also provide the money that those markets use in final settlement is much harder to say, though I’m a firm believer it will not.

Take Your Pick

So, where does all this leave us? I don’t have a crystal ball, but I do think the idea of money becoming more closely linked to the community it serves is a powerful notion. And, since we all belong simultaneously to multiple, overlapping communities, we’re probably not heading toward a single global currency. Instead, it’s looking like we’re in for a world of currencies.

How We Get To Next was a magazine that explored the future of science, technology, and culture from 2014 to 2019. This article is part of our Made of Money section, which covers the future of cash, finance, economics, and trade. Click the logo to read more.